In Florida, Skyrocketing Insurance Rates Test Resolve of Homeowners in Risky Areas

ALTAMONTE SPRINGS, Fla.—For most of his life, Cory Infinger has lived down a hill and along a bend in the Little Wekiva River, a gentle stream meandering northwest of Orlando. During Hurricane Ian, in September 2022, the stream swelled, inundating the homes of his family and his neighbors and also the street where they live, making it impassable.

Overnight Ian had moved slowly and violently over the state’s interior, dropping historic amounts of rain, after coming ashore in southwest Florida as a category 4 hurricane, its high winds and storm surge flattening coastal communities there.

For Infinger the deluge forced a hasty morning evacuation with his wife and youngest two of their three children. It would displace the family for months as their home underwent massive repairs. More than a year later the ordeal has left the family rattled, especially his 16- and 8-year-old children, said Infinger, who grew up fishing and trapping turtles along the Little Wekiva and now enjoys doing the same with his kids. (A 22-year-old son no longer lives at home.)

“You could tell they were sad when we came back to get the last few things,” he recalled of his kids as he described the family’s temporary stay in a rental house, and then the move back to their newly remodeled home. “It took them a while to get used to, this is our new house. Everything had changed.”

In the last seven years Florida has weathered five major hurricanes. Michael, which made landfall in 2018 in the Panhandle, was the first category 5 hurricane to strike the continental United States since Andrew in 1992. Ian, in 2022, was the costliest hurricane in state history and third-costliest on record nationwide, after Katrina in 2005 and Harvey in 2017. Recent major Florida hurricanes also include Irma in 2017, Nicole in 2022 and Idalia in 2023.

If the disasters sharpened Floridians’ resolve, in the immediate aftermath, to build back stronger and better, another crisis may be causing some to rethink where they live and the rising risk as the global climate warms.

After Ian, Infinger’s taxes and homeowners insurance, which he pays together into a bank escrow account as part of his regular mortgage payment, jumped by $450 a month. That amount could be considered moderate in a state where annual home insurance rates in the five and six figures have not been unheard of in recent years, and many homeowners have received letters from their insurers informing them that their existing policies will not be renewed.

Some homeowners have received multiple such letters from multiple insurers, leaving them scrambling from one policy to the next, as lenders require mortgage-holders to carry insurance. Others whose homes are paid off are going without insurance altogether, to spare the expense.

“We deal with it,” said Infinger, who, with his wife, is considering moving away from the Little Wekiva in the coming years. For now, he said, “there’s nothing really we can do about it.”

We’re hiring!

Please take a look at the new openings in our newsroom.

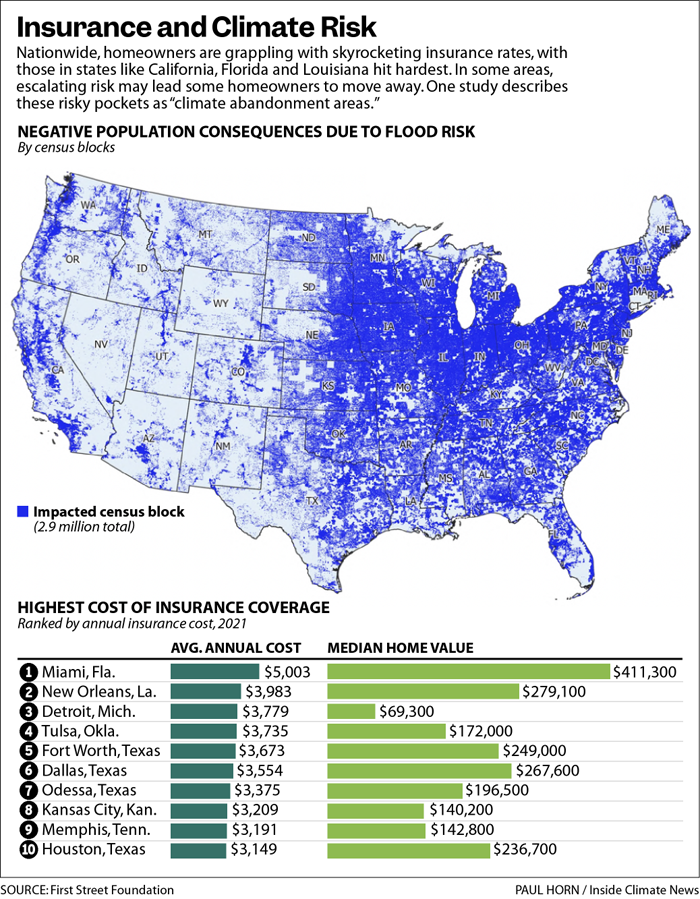

See jobsAcross the country homeowners are grappling with skyrocketing insurance rates and dropped policies, with those in states such as California, Florida and Louisiana hit hardest. Growing evidence suggests the soaring costs only hint at the widespread unpriced risk facing homeowners as the warming climate leads to rising seas and more damaging hurricanes and wildfires.

As many as 6.8 million properties nationwide have been affected by insurance problems, but that number represents a fraction of the 39 million homes and businesses vulnerable to flooding, hurricanes and wildfires whose risk has not been priced into their policies, according to a study by the First Street Foundation, a nonprofit researching climate risk. Together these 39 million properties constitute what the study characterizes as an “insurance bubble,” defined by properties likely overvalued because of underpriced or subsidized insurance.

Other research suggests the changing climate has not been priced into the real estate market in a way that reflects the risk. A separate study published last year in Nature Climate Change, a peer-reviewed journal, estimates that residential properties vulnerable to flooding are overvalued by $121 billion to $237 billion, in part because of the subsidized National Flood Insurance Program.

The study found that the most overvalued properties are concentrated in coastal counties where there are no flood risk disclosure laws and where there is less personal concern about climate change. Much of the overvaluation is driven by properties situated outside of the 100-year flood zones designed by the Federal Emergency Management Agency. Low-income households especially are in danger of losing home equity, potentially leading to wider wealth gaps. In Florida properties are overvalued by more than $50 billion, according to the study.

The unpriced risk is important for many reasons. Municipalities that rely on property tax revenue may be vulnerable to potential shortfalls, the study says. The National Climate Assessment pointed out last year that the overvaluation of coastal properties makes it difficult to move people out of harm’s way, because of the limited amount of compensation available through flood insurance and federal flood disaster assistance programs.

“Florida is one of the riskiest places from a climate impact standpoint that you can live in,” said Rob Moore, director of the flooding solutions team at the Natural Resources Defense Council. “One only needs to look through a few years of front pages to see how many major hurricanes have struck this state, and that definitely had an impact on how both private insurers and insurers in the public realm are looking at risk and pricing it in the state of Florida.”

“We’re so far behind in regard to pricing in the climate. That’s why we’re seeing these big (insurance) spikes in places like Florida and California and Louisiana,” said Jeremy Porter, head of climate implications research at the First Street Foundation. “It’s the first mechanism to start to price climate into the housing market.”

Insurance Rates Soar

The United States experienced a record 28 billion-dollar disasters in 2023, a year that was characterized by historic extreme heat across much of the country, according to the National Oceanic and Atmospheric Administration. The disasters included the Maui wildfire that was the nation’s deadliest in more than a century and Hurricane Idalia, the strongest hurricane to make landfall in northwest Florida since 1896. The data show a clear upward trend in the number of severe events each year. The previous record of 22 disasters was set in 2020.

The best way homeowners can protect themselves from risk is with insurance, and there are several reasons why rates are climbing, including inflation and changes in government regulations, along with growing exposure. The skyrocketing rates add to the cost of owning a home, and when the rates reach a point where they are unaffordable, that can affect the homeowner’s ability to make the mortgage payments. In high-risk areas where affordable rates are scarce, that can affect market demand, and home values may begin to decline.

“People want to live on the ocean,” said Mark Friedlander, spokesman for the Insurance Information Institute, a New York-based industry organization. “People want to live on the coastlines. Eighty percent of Florida’s population lives in coastal counties. People want to live where they can be at the beach in 20 minutes, and even when we have a catastrophic event like a hurricane, people want to rebuild.”

“It’s very clear to us that the cost and availability of insurance in Florida will have a detrimental impact on a very vibrant real estate market here,” he said.

Most notably, the government-backed National Flood Insurance Program has raised rates nationwide under its new pricing methodology, Risk Rating 2.0. The change represents a shift away from the subsidization that had helped transfer risk away from homeowners, toward premiums that are more commensurate with risk.

In 12 states, flood insurance premiums have doubled, although no part of the country has been untouched, with rates in Florida jumping by 231 percent, Kentucky by 207 percent, Louisiana by 234 percent, South Dakota by 207 percent and West Virginia by 272 percent, according to the First Street Foundation study. This appears to have led some homeowners to forgo insurance altogether, as the number of policies in force has dropped by 21 percent to 4.7 million.

“That does price in climate risk in a way that it didn’t for the last 50 years,” Porter said.

Meanwhile states are responsible for regulating their own insurance markets, to avert situations where insurers can exploit vulnerabilities in the market and raise rates unreasonably. But some regulations may prevent insurers from setting rates that reflect the risk, and in some areas insurers are struggling to offer affordable policies that are actuarially sound. In California this has led insurers to limit or withdraw coverage in high-risk areas. Some areas have experienced a nearly 800 percent increase in the number of policies that insurers have not renewed, driving homeowners to the state-run insurer of last resort, the FAIR Plan.

A similar situation has developed in Florida, Moore said. Since Hurricane Andrew hit south Florida in 1992, a growing number of large insurers have left the state.

“Private insurers realized holy cow, we have a lot of exposure in the state of Florida. We have to increase premiums if we’re going to do business here, and the state didn’t want to do that,” he said. “It could slow development down.”

Regionally focused insurers moved in, and the recent spate of hurricanes forced some to go under, driving homeowners to Florida’s insurer of last resort, Citizens Property Insurance Corporation. Friedlander said other factors also have contributed to Florida’s insurance crisis, including an extreme number of lawsuits against insurers. Governor Ron DeSantis has implemented reforms aimed at addressing the litigation.

Today, Citizens is Florida’s largest insurer. The number of policies in force has climbed by 168 percent from under 500,000 to more than 1.3 million, and the average premium has climbed by 61 percent from $2,000 to $3,300, according to the First Street Foundation study. Inland areas are especially affected. In the Orlando area the number of policies in force in Seminole County has jumped by 2,992 percent, in Orange County by 2,818 percent and in Osceola County by 2,491 percent. The largest increase in the number of policies is in Miami-Dade County, which added nearly 125,000 between 2016 and 2023.

This heavy reliance on Citizens affects all Floridians, even those without any need for homeowner’s insurance. State regulations limit how much Citizens rates can rise, and because the insurer is backed financially by the state, if a particularly destructive event were to occur, such as a major hurricane or series of storms in a single season, there is a chance Citizens’ budget would not be enough to cover the losses, and the costs would become the burden of the state.

Citizens is in the process of downsizing its number of policies, and private insurers are taking some of them on. Meanwhile, Florida’s insurance regulator has approved six new insurers to begin operating in the state in 2024. One of them already is in business, and the increased competition may help stabilize rates and ease the exposure for Citizens.

“There’s Just No Easy Solutions”

DeSantis’ latest budget proposal calls for tax exemptions for insurance costs and funding for resiliency planning and projects. The proposal also puts money toward helping Floridians harden their homes against climate impacts. Florida lawmakers are taking up the budget proposal during their annual legislative session, which concludes March 8.

There also have been a few bills this session aimed at the insurance crisis, including one that would remodel Citizens after the National Flood Insurance Program, except that Citizens would offer windstorm insurance. Citizens’ Chief Executive Officer Tim Cerio testified during a legislative workshop that the measure could cause the insurer’s reinsurance to skyrocket, and the bill has not advanced.

The First Street Foundation study points out that insurers could offer discounts to homeowners who take steps to fortify their homes, which would help make disasters less damaging. Moore said Florida once was a leader when it came to measures like building codes, although that has changed in recent years. The state also had lacked a disclosure policy requiring property owners to share a property’s flood history with buyers and renters.

Another bill would compel landlords to inform tenants that they live in a flood zone, and yet another would force home sellers to disclose past flooding and insurance claims to potential buyers. The first measure has not advanced. The second was approved Monday by the House and Senate and heads next to DeSantis for his signature.

“We’ve got to stop putting more and more people in harm’s way, especially in Florida where we could see a foot or two-and-a-half feet of sea level rise in the next 30 years, over the term of a 30-year mortgage. Maybe we should tell people that before they buy a house. Maybe we don’t issue that permit to build the house there in the first place. There’s a revolutionary idea for the state to consider,” Moore said.

“As long as the state of Florida is determined to keep people in the dark about the risks, they are reaping the seeds they have sown,” he said. “All you have to do is look at the development boom in some of the riskiest areas of the state.”

Escalating risk may lead some homeowners to abandon certain areas. A separate study from the First Street Foundation combines Census Bureau and flood risk data to identify what the study describes as “climate abandonment areas,” where population declines between 2000 and 2020 can be linked with vulnerability.

The areas are scattered nationwide but concentrated along most of coastal Florida, the Mid-Atlantic region between New Jersey and Washington, D.C., and the Gulf Coast of Texas, especially in Houston. The areas can be found even in some of the fastest-growing metropolitan areas, like Miami. In Miami-Dade County, properties lost as much as $3.99 per square foot in home value due to flood risk between 2005 and 2017, according to the study.

“As long as the state of Florida is determined to keep people in the dark about the risks, they are reaping the seeds they have sown.”

Such migrations likely would not be consistent and would be tied with socioeconomic means. Buyout programs are small compared with the widespread risk, Porter said.

Moore said providing relocation assistance has proven challenging in various places across the country. It can take time for the assistance to reach the person, and it can be difficult to help the person get to where he or she wants to go, he said.

“Most of our energies are about buying them out so they can go somewhere else. But where else they go, it also presents some challenges as well, especially in fast-growing areas where property values are growing,” he said. “That may not be enough to help them relocate to a safer place.”

“There’s just no easy solutions to this, and solutions are exponentially harder in a state that’s determined to continue development in high-risk areas,” Moore said. “There are no solutions that are going to work long-term when that’s the dynamic at play.”

Added Friedlander: “We don’t see the (insurance) market getting worse. But unfortunately what does that mean for the average consumer? It does not mean the bill is going down today or tomorrow. We’re talking about a stabilizing market. We’re hoping in 2024 we will see more moderate rate increases than we’ve seen before, but we can’t predict.”

A Rare Spot of Nature

For Infinger, his family’s property along the Little Wekiva represents a rare spot of nature tucked away within the urban web of highways and subdivisions outside of Orlando.

He speaks with wonder rather than worry as he recalled a time when he and his wife watched a bear through a window of the family home, as the animal made a snack of acorns. Of observing coyotes come and go through the yard. He grew up with some of his neighbors. This feels like home.

That may change, though. The family has the money to pay the escalating insurance rates, said Infinger, 41, who works in construction. But as their kids get older, he and his wife are making plans to move farther outside of Orlando, closer to his parents. He fears his beloved Little Wekiva will flood the low-lying family home again in the future.

“We already know it’s going to flood,” he said. “It’s just a matter of time.”

Share this article

Disclaimer: The copyright of this article belongs to the original author. Reposting this article is solely for the purpose of information dissemination and does not constitute any investment advice. If there is any infringement, please contact us immediately. We will make corrections or deletions as necessary. Thank you.